Greenhouse gas emissions from burning US-sourced woody biomass in the EU and UK

Summary of research findings Environment and Society Programme, October 2021

Introduction

As more and more countries adopt climate targets to achieve net zero greenhouse gas emissions, the relevance of forests as stores of sequestered carbon has increased. However, the growing use of forest biomass to generate electricity and heat has raised concerns over the immediate emissions resulting from burning wood.

Many national and intergovernmental policy frameworks, including those of the EU and UK, currently treat biomass energy as zero-carbon at the point of combustion. Accordingly, they grant it access to financial and regulatory support available for other renewable energy sources. These incentives have driven a rapid increase in the consumption of biomass for energy, even though its combustion may increase atmospheric concentrations of carbon dioxide (CO₂) for years or even decades to come.

This report examines the issue in relation to one particular source of woody biomass: wood pellets sourced from the US that are burnt for electricity and combined heat and power (CHP) in the EU and UK. Although wood pellets represent only a proportion of the total woody biomass consumed for energy in the EU–and of forest harvests in the US–the market has grown rapidly in recent years. US-sourced pellets account for the majority of wood pellet imports to the UK and are an important source for the EU.

In 2019, according to our analysis, US-sourced pellets burnt for energy in the UK were responsible for 13 million–16 million tonnes of CO₂ emissions, when taking into account emissions from their combustion and their supply chain, forgone removals of CO₂ from the atmosphere due to the harvest of live trees and emissions from the decay of roots and unused logging residues left in the forest after harvest. Almost none of these emissions are included in the UK’s national greenhouse gas inventory; if they were, this would have added between 22 and 27 percent to the emissions from total UK electricity generation, or 2.8–3.6 percent of total UK greenhouse gas emissions in 2019. This volume is equivalent to the annual greenhouse gas emissions from 6 million to 7 million passenger vehicles.

Emissions from US-sourced biomass burnt in the UK are projected to rise to 17 million–20 million tonnes of CO₂ a year by 2025. This represents 4.4–5.1 percent of the average annual greenhouse gas emissions target in the UK’s fourth carbon budget (which covers the period 2023–27), making it more difficult to hit a target which the government is currently not on track to achieve in any case.

While emissions are likely to fall by 2030, with the end of government support for power stations converted from coal to biomass, they could rise again thereafter if bioenergy with carbon capture and storage (BECCS) plants are developed at scale.

Greenhouse gas emissions from biomass for energy

Wood may be used for energy in several different forms. The impact on the climate of burning wood feedstocks is very different for each of these forms. However, categories used for reporting consumption by energy companies do not distinguish accurately enough between stemwood from harvesting whole trees and residues from sawmills or harvesting operations for other purposes.

Burning biomass for energy creates a significant initial increase in carbon emissions, which is only balanced by regrowing trees and the displacement of fossil fuels. Depending on the feedstock used and the efficiency of combustion, the net impact is to increase global warming for, at best, one–two decades and, at worst, centuries. This ‘carbon payback period’ matters because CO₂ emissions are higher during this period than they would otherwise have been. Although the CO₂ should eventually be absorbed, the elevated levels in the interim are likely to be incompatible with the 2015 Paris Agreement on climate change’s aim of peaking global emissions ‘as soon as possible’. They also increase the risk of reaching a climate tipping point, when a small rise in global temperature prompts a large and potentially irreversible change in the global climate.

The smallest impacts on the climate–i.e. the shortest carbon payback periods–derive from the use of residues and wastes from forest harvesting or forest industries that imply no additional harvesting and would otherwise be burnt as waste or left to decay, thereby releasing carbon to the atmosphere in any case. Typical examples of such wastes are sawmill residues and black liquor (a waste product from pulp and paper mills). The impacts on the climate of forest residues that would otherwise have been left to rot on the forest floor depend partly on their decay rates, which vary significantly according to local climatic conditions.

The most negative impacts on carbon concentrations in the atmosphere derive from increasing harvest volumes or frequencies in already managed forests, from the harvesting of natural forests or their conversion into plantations, or from displacing wood from other uses, for example panels or particleboard. Where whole trees are harvested and used for energy, not only is the carbon stored in those trees released to the atmosphere immediately, but the future carbon sequestration capacity of those trees is lost. It takes time for the growth of unharvested trees or replacement trees to compensate. Naturally regenerated forests tend to be older and have larger trees when harvested than plantation forests, which have higher growth rates and are typically harvested earlier. Therefore, more stored carbon is lost when natural forests are harvested and the carbon emitted takes longer to replace.

On the other hand, in the absence of active forest management, the incidence of dead and diseased trees increases and the rate of net carbon absorption by most forests falls. Over time the forest may also become more vulnerable to wildfires and other disturbances. There can, therefore, be benefits to the climate over the long term from some level of management and harvesting.

Claims are sometimes made that demand for wood for energy provides additional income to landowners, encouraging them to maintain and possibly even to expand their forests, rather than allow them to be cleared. Such claims are based on economic theory and are not consistent with the empirical evidence, which suggests the opposite: that increased demand for wood for energy prompts growth in the total area and volume harvested, leading to a reduction in the forest carbon store.

Similarly, it is sometimes claimed that the practice of thinning–the removal of selected trees or rows either to allow stronger growth in remaining trees or to reduce fire risk–can increase forest carbon storage. Almost all of the studies on which this claim rests focus on volume growth in remaining trees, conclude that this does not lead to an increase in total stand volume compared with an uncut stand, and do not report statistics about carbon uptake by the ecosystem. More recent studies have shown that the use of thinnings for energy does not reduce net greenhouse gas emissions for years at best, and can, under some circumstances, increase them. In general, intact forests with high tree-species diversity, largely free from human intervention, are the most carbon-rich ecosystems, with higher rates of biological carbon sequestration.

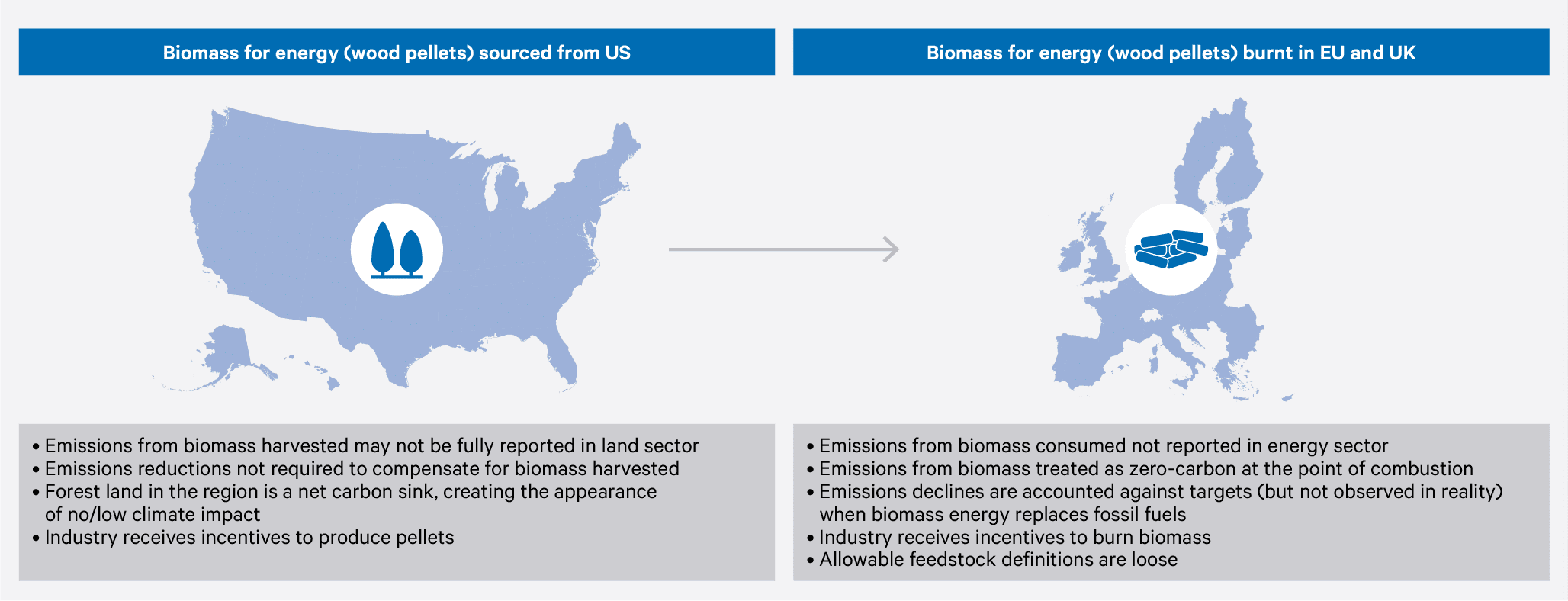

A fundamental reason why biomass is treated by policy frameworks as zero-carbon at the point of combustion is because emissions from biomass consumption for energy are reported not in the energy sector of national reports under the UN Framework Convention on Climate Change (UNFCCC), but rather in the land-use sector of the country in which the biomass is harvested (in order to avoid double-counting). This approach was adopted for the limited purpose of counting global emissions through reporting, but it has fed through into national accounting–measuring emissions levels against countries’ targets under the 1997 Kyoto Protocol, the Paris Agreement or national legislation, such as the UK’s Climate Change Act. This causes a particular problem where the countries producing and consuming the biomass are not the same. When importing countries replace fossil fuels with biomass for heat and power, their emissions totals fall immediately, but there is no automatic mechanism to ensure that the exporting countries reduce their emissions in other sectors to compensate for the loss of sequestrated carbon.

Attempts to address these issues under the Kyoto Protocol were not wholly successful, and the problem is unlikely to be resolved under the Paris Agreement either. Most nationally determined contributions (NDCs) submitted so far under the latter do not contain separate targets for the land-use sector; relatively few anticipate the use of any kind of accounting rules; and where accounting for land-use sector emissions and removals is mentioned, the submitting countries have chosen a variety of accounting methods. As a result, it is not possible to assess the net climate effects of bioenergy simply by comparing the emissions from combustion with those associated with feedstock in the land-use category and supply chain. Therefore, there is no automatic link between falling emissions in countries consuming bioenergy and the need for corresponding action in the countries supplying the feedstock.

In any case, even if the figures could be accurately estimated and the accounting challenges overcome, the point remains that by treating biomass emissions as zero at the point of combustion, a significant incentive is created for consuming countries to burn wood for energy, despite CO₂ emissions increasing relative to fossil fuels for a period of decades or centuries as a result.

The incentives are greater still at the industry level. In the UK and most EU member states, energy companies are paid to burn biomass and face no responsibility to compensate for the associated emissions elsewhere. Reporting of higher land-use emissions by countries of origin would have no bearing on the activities of these companies, and even if some mechanism could be devised to create a linkage with emissions in the country of origin, current policy frameworks in consuming countries would still lead to higher CO₂ levels in the atmosphere for the duration of the carbon payback period than would have occurred in the absence of support for burning biomass. Figure S1 below summarizes these arguments.

Figure S1. The problem of missing emissions

Source: Compiled by the authors

1 The UK officially left the EU on 31 January 2020, thereby reducing the number of EU member states to 27. However, this summary includes several references to the former EU28—which includes the UK—as the relevant data covers the period prior to that date.

US-sourced biomass in the EU and UK: consumption and associated emissions

For the last ten years, the former EU281 has been the main global source of demand for wood for modern (non-traditional) uses of biomass for power and heat, a result largely of the policy support frameworks put in place by EU member states following the 2009 Renewable Energy Directive. Biomass is the largest single source of renewable energy, accounting for 60 percent of gross consumption in 2018. Solid biomass (almost all wood) by itself accounted for 41 percent. Within the former EU28, the UK saw the greatest growth in the use of biomass for electricity, in absolute terms. In 2018, the UK accounted for 24 percent of all electricity generated from biomass in the EU.

The EU is a major producer of wood for energy and the world’s largest producer of wood pellets. Total consumption of wood for energy is higher than production, however, so the EU is a net importer, mainly of wood pellets. In 2018 the former EU28 produced 16.9 million tonnes of wood pellets and imported 10.3 million tonnes; about 60 percent of the latter came from the US. The UK has been by far Europe’s (and the world’s) biggest consumer: in 2018 it consumed an estimated 8.3 million tonnes, representing 21 percent of all the wood pellets produced worldwide. The Drax power station alone burnt 7 million tonnes of pellets in that year. Alongside the UK, Belgium, Denmark and the Netherlands import significant quantities of wood pellets from the US.

While emissions from the combustion of biomass are not included in nationally reported emissions from energy, they are recorded in reports to the UNFCCC. Analysis of these reports show that while energy-related emissions across the former EU28 were reported as falling by 26 percent between 1990 and 2019, if emissions from bioenergy (from all sources, solid, liquid, and gaseous) had been included, the reduction would have been 15 percent. In the UK, while the emissions decrease between 1990 and 2018 was 38 percent, if emissions from bioenergy had been included, the reduction would have been just 32 percent. (These figures relate only to emissions from burning the biomass; they do not include life cycle emissions reflecting changes in forest carbon stock.)

The paper analyses emissions from the consumption of US-sourced biomass in the EU and UK under three headings: emissions from pellet combustion; emissions from energy use in the supply chain; and forgone removals of CO₂ from the atmosphere and emissions from the decay of roots and unused logging residues. Our analysis shows that, across these three categories, emissions from the use of US-sourced wood pellets for energy in the EU28 increased from 9 million–11 million tonnes of CO₂ in 2014 to 16 million–19 million tonnes in 2019. Most of this was accounted for by the UK, where emissions increased from 7 million–8 million tonnes of CO₂ in 2014 to 13 million–16 million tonnes in 2019. Almost all of this UK increase was associated with biomass burnt at Drax.

Future growth of biomass energy and associated emissions in the EU and UK

Projections for the future use of woody biomass sourced from the US and used for energy within the EU27 indicate that imports to Denmark and the Netherlands will grow into the mid to late 2020s, while imports to Belgium remain roughly constant. By 2030 demand is projected to fall, owing to the gradual withdrawal of government support in the consuming countries. We estimate that total demand for US wood pellets in the EU27 will grow from 1.3 million tonnes in 2019 to about 3.5 million tonnes in 2025, before then falling to 2.0 million tonnes in 2030. This represents an increase from 3 million–4 million tonnes of associated CO₂ emissions in 2019 to 8 million–10 million tonnes in 2025, before falling back to 5 million–6 million tonnes in 2030.

However, these figures may prove to be underestimates if further coal-to-biomass conversions in other member states, particularly in Germany, move forward. Such converted stations would have the potential to almost triple EU27 wood pellet consumption compared with 2018 levels. Most of the countries where coal-to-biomass conversions are likely to take place are not currently major importers from the U.S., but should supplies from domestic or EU sources, or other major exporters, become constrained, the US could become a supplier to them too.

EU projections for growth in bioenergy beyond 2030 rely partly on a huge increase in energy crop production within the EU. Should this fail to materialize (policy frameworks do not currently support it), this could further increase demand for more well-established feedstock, mainly wood. Demand may also be generated, from the 2030s into the 2040s, by the development of BECCS plants.

In the UK, demand for US-sourced wood pellets from existing coal-to-biomass conversions (the Drax and Lynemouth power stations) will remain high until 2027, when government support is due to end. (It is possible that Drax will lobby for the continuation of subsidies, particularly if support for BECCS is promised in the 2030s.) When the MGT Teesside Tees Renewable Energy Plant currently under construction comes on stream, demand will rise further, as its subsidies are due to last for 15 years. Additional demand may arise from the expansion of biomass for heat, which is more likely to be used for industrial purposes than for residential. Most significantly, further demand could come for the development of BECCS technology. Each of the scenarios developed by the UK’s Climate Change Committee to illustrate how the UK could meet its net zero emissions target by 2050 rely on BECCS to a greater or lesser extent, and in most cases rely on imports, even if ambitious targets for the expansion of UK forestry and energy crops are achieved.

We estimate that demand for US wood pellets in the UK will grow from 5.5 million tonnes in 2019 to 7.0 million tonnes in 2025, before falling to about 2.9 million tonnes in 2030. (This assumes that current subsidies end as planned in 2027.) Emissions are projected to rise from 13 million–16 million tonnes of CO₂ in 2019 to 17 million–20 million tonnes in 2025, before dropping to 7 million–8 million tonnes in 2030. (These projections assume that only one of Drax’s four biomass units remains operational in 2030. If more are kept running–e.g. for energy security reasons or in anticipation of future subsidies for BECCS plants–emissions in 2030 could be higher, ranging from 15 million–18 million tonnes for all four units.)

Conclusions and recommendations

The treatment of biomass as zero-carbon in policy frameworks has led governments to provide significant financial and regulatory support for the use of biomass for power and heat. Since emissions take time to be reabsorbed by forest growth, carbon emissions in the atmosphere will increase for a period of decades or even centuries, depending on the feedstock type. Policymakers in consumer countries will be given a false sense of optimism about the progress being made in decarbonizing their energy supply, while producing countries have no corresponding incentive to reduce future emissions in compensation. Subsidies for biomass energy have been delivered–and seem likely to continue–with essentially no mechanism to discriminate between feedstocks with different carbon payback periods, and therefore no effective means of limiting the impact on the climate.

The type of feedstock used in biomass plants is critical. We conclude that only those categories of feedstock with the lowest carbon payback periods should be eligible for financial and regulatory support. This is consistent with the Paris Agreement’s aim of peaking global emissions ‘as soon as possible,’ and reduces the chance of reaching a climate tipping point.

The current sustainability criteria in the EU and UK that define the categories of biomass feedstock that can be supported and the conditions under which they can be burnt do not take account of the real impacts of different feedstocks on the climate and cannot, accordingly, achieve this aim. They are also defective in other ways. (If adopted, the new proposals published by the European Commission in July 2021 would improve EU sustainability criteria somewhat, but their impact would be very limited.) We therefore recommend that EU and UK sustainability criteria be amended as follows:

Only those categories of feedstock with the lowest carbon payback periods should be eligible for support: sawmill and small forest residues and wastes with no other commercial use whose consumption for energy does not inhibit forest ecosystem health and vitality.

- Much tighter definitions of feedstock categories should be introduced to prevent whole trees being treated in the same way as genuine residues.

- Periodic monitoring of feedstock use and impact should be conducted to ensure that allowable feedstocks are not diverted from other uses–e.g. for wood products.

- Additional criteria should be included to protect particular types of landscape, including primary and highly biodiverse forests, from the extraction of biomass for energy. (This is included in the European Commission’s new proposals.)

- The UK’s adoption of a ceiling on feedstock supply chain emissions of 29 kg CO₂eq/MWh is welcome in limiting the types of feedstock that can be used; it seems likely to restrict feedstocks to domestically sourced products. Similar limits should be introduced in the EU.

- The energy efficiency thresholds for new power stations in the EU criteria should be increased and extended to both older and smaller installations.

- The new proposals from the European Commission to extend support beyond 2026 for the use of forest biomass in electricity-only installations in coal-dependent regions will encourage further coal-to-biomass conversions and should be dropped.

- Feedstock for BECCS plants should be subject to at least the same constraints as other biomass plants.

Emissions from any type of biomass used for energy not satisfying the criteria proposed above should be included in full in the consuming country’s greenhouse gas totals when judging progress against their national targets and in relevant policy frameworks, such as the EU’s Emissions Trading System. Since these categories of feedstock have longer carbon payback periods than those eligible for support under our recommendations, this would be an effective way of ensuring that the period during which carbon concentrations in the atmosphere are higher than they would otherwise have been is not simply ignored, as it is under existing policy frameworks.