The insurance industry isn’t built to keep up with rising floods

Climate change is raising your flood insurance rates, but not how you might think

Archival photograph of extreme flooding in Alabama in 1916.

photo by Steve Nicklas, NOS, NGS

Flooding is a hallmark of the climate-changed world. Rising sea levels, extreme rainfall, and aging infrastructure systems have left communities across the U.S. facing increasing damages from flooding, making flood insurance an expensive necessity for more and more Americans.

But U.S. flood insurance policy was created on the assumption of a more stable and predictable climate and has struggled to keep up with the rapid pace of change. Two new papers led by Research Associate Dominick Dusseau shine a light on vulnerabilities within the American flood insurance system that will only be exacerbated as climate change advances.

You may be paying for your neighbor’s discount

The National Flood Insurance Program (NFIP), a program of the Federal Emergency Management Agency (FEMA), was created to help property owners secure affordable flood insurance and encourage communities to manage their flood risk.

One of the ways the NFIP encourages floodplain management is through the Community Rating System. The system rewards communities with discounts on their premiums for implementing certain actions. These actions range from building up the elevation of ground within a floodplain to making local flood maps publicly accessible. Actions are assigned points and the number of points determines how much of a discount the community will receive.

This reduction in price is not a true discount however, because the NFIP adjusts state-wide premiums to make up the difference. The NFIP calculates the average percentage discount for the entire state and increases all premiums by that amount. This means policyholders in towns that are not even participating in the Community Rating System may be paying more than their risk level requires to subsidize their neighbor’s discounts.

“It’s basically a way for the NFIP to actuarially pay for the Community Rating System,” says Dusseau. “Because otherwise they’d be foregoing that revenue from the discounts. To recoup the lost income they do this cross-subsidization by putting it back into each policy by state. ”

Climate change will exacerbate inequalities

A study from Dusseau, published in the journal One Earth, shows that through the Community Rating System, roughly half of NFIP policyholders subsidize the discounts of the other half. In theory, subsidization ensures the NFIP is collecting enough revenue to pay out all their future obligations. But in reality, this framework presents two flaws. First, not all Community Rating System actions—publishing flood maps, for example—reduce damages. While the action may be beneficial to community awareness, it doesn’t translate directly to dollars saved.

Additionally, existing disparities between communities result in unequal distribution of the burden of subsidization.

States with the greatest level of inequality now will experience even worse disparities in the future.Dominick Dusseau

“One of the big takeaways that we found was that it’s largely under-resourced rural counties that are subsidizing the more affluent, well-resourced urban counties,” says Dusseau.

Even though many rural communities would be eligible for discounts themselves, they may not have the capacity available to take advantage of them.

“There’s a bureaucracy involved here. There’s paperwork. You have to document all of these things that you’re doing. You have to submit the application. You need someone that’s a certified floodplain manager,” says Dusseau. “Not every town has that capacity, so it just falls through the cracks.”

This means that already resource-strapped communities may be paying more than required for their true risk level.

Dusseau’s study points out that these inequalities will be exacerbated by climate change. The NFIP has long underpriced policies. The rising sea levels and more extreme precipitation caused by climate change has only widened the gap between the program’s revenue and obligated pay-outs. In 2021, FEMA implemented a new framework, called Risk Rating 2.0, that takes the impacts of climate change to date into account, gradually raising premiums year over year to more closely align with the actual risk of damages.

“And what we see is that states with the greatest level of inequality now will experience even worse disparities in the future,” says Dusseau.

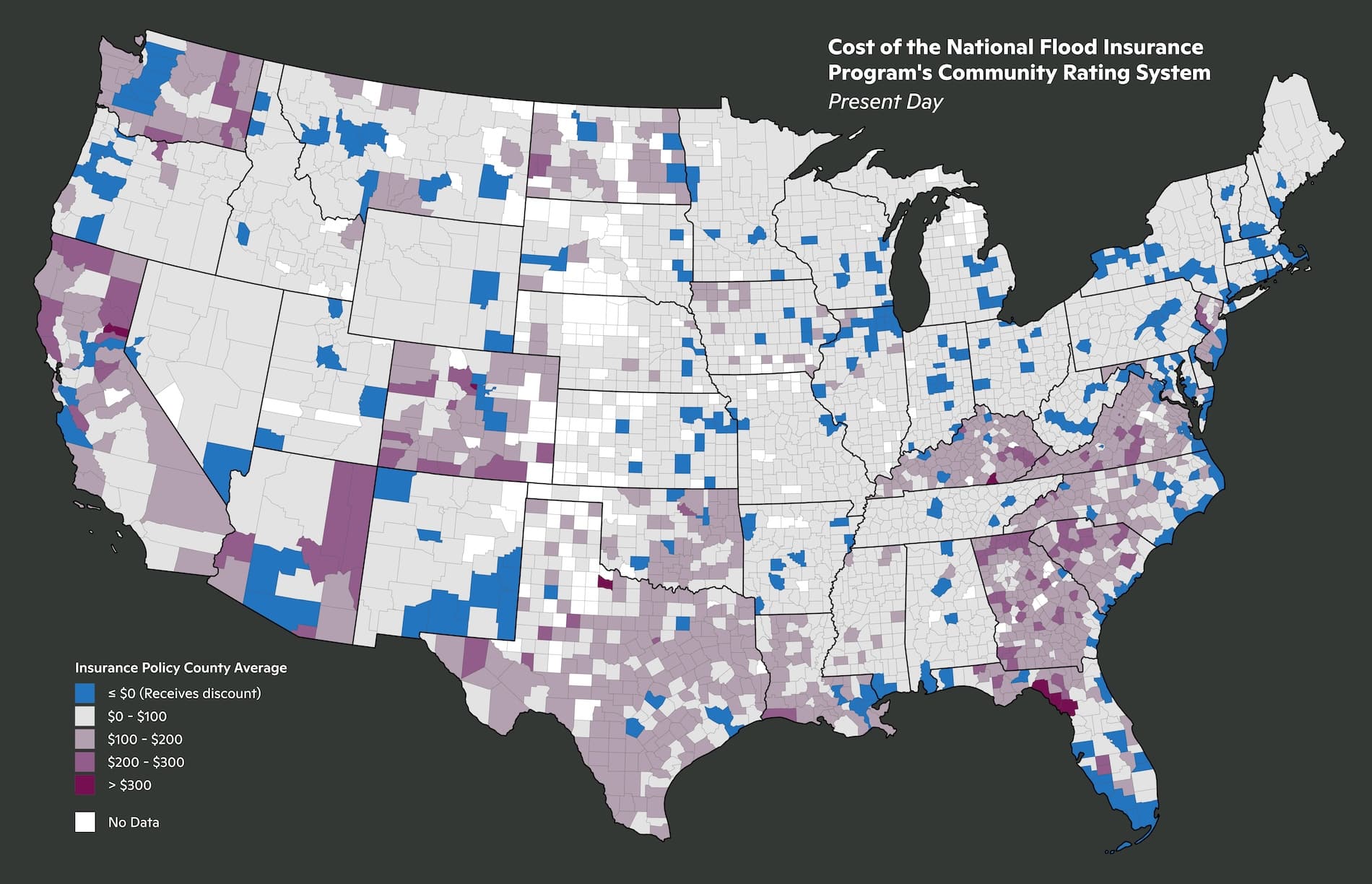

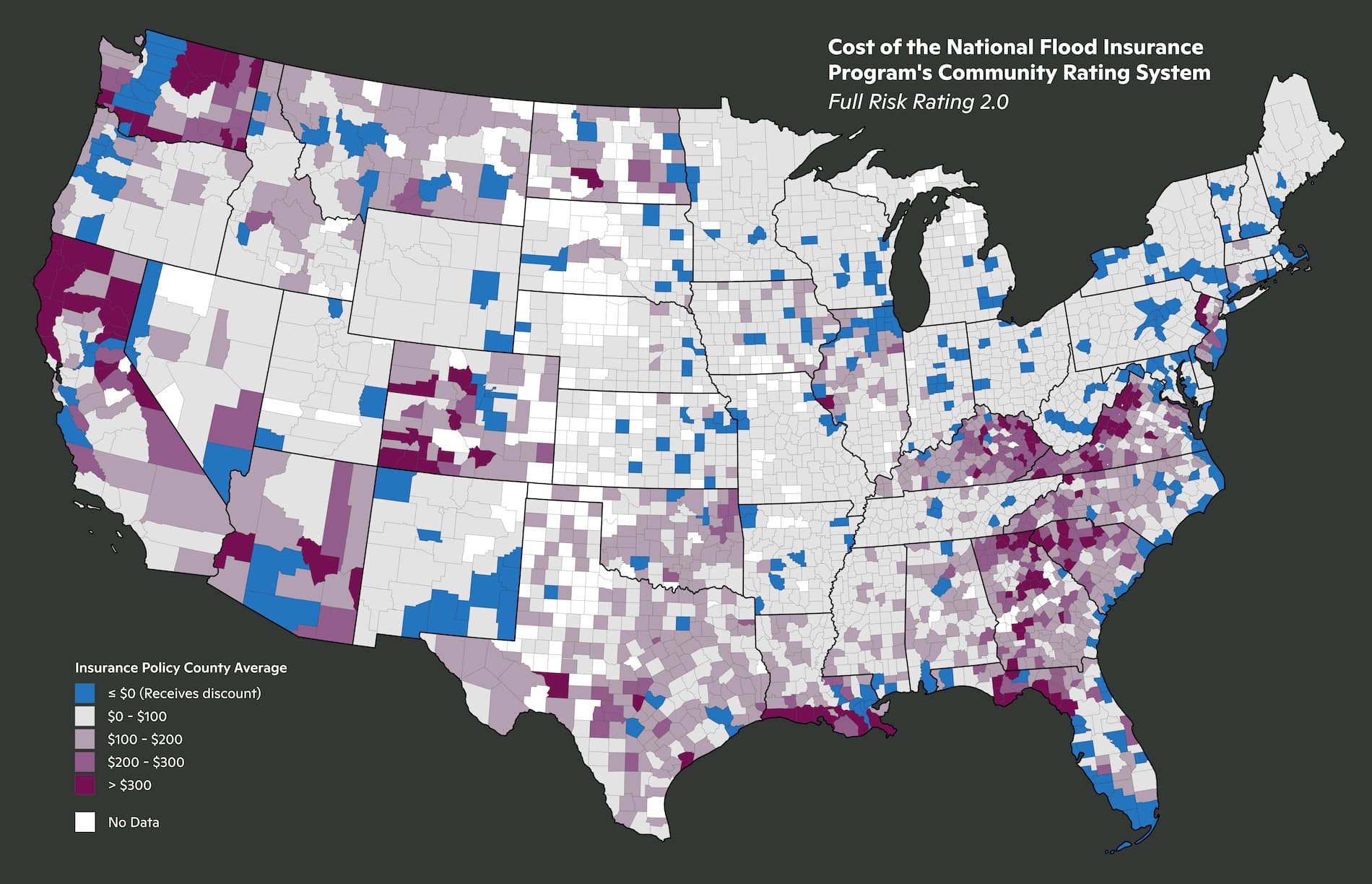

(top) Current day costs by county of the Community Rating System.

(bottom) Costs under the Risk Rating 2.0 framework.

maps by Dominick Dusseau

How accurate are flood models?

In addition to inequity, flood insurance suffers from a frustrating lack of transparency, with each company and the NFIP employing a proprietary combination of models to decide premium prices. A second paper led by Dusseau, published in the Journal of Catastrophe Risk and Resilience in February, generates some much needed transparency around the data underlying the insurance industries assumptions.

One type of model employed by insurers is called a catastrophe model. These models can estimate the likely damages from both natural and man-made hazard events like wildfires, terror attacks, and hurricanes. Dusseau’s study evaluated the accuracy of seven flood-specific catastrophe models, including three commonly used by the NFIP.

“Insurers rely heavily on these models that have historically been very ‘black-box’—nearly impossible to evaluate their methods,” says Assistant Scientist Zach Zobel, a co-author on the paper. “Without proper independent review of these models, insurers will continue to misrepresent the risk catastrophes pose on local communities.”

Flooded area of Venice, LA after Hurricane Katrina.

photo by Lieut. Commander Mark Moran, NOAA Corps, NMAO/AOC

The study found that model accuracy varied widely. Some models overestimated flood losses, while others underestimated losses— by up to 13 times in the most extreme case. This has major implications for the ultimate cost of flood insurance.

“There is a non-trivial difference in the premiums that would be passed on to consumers based on these assumptions,” says Dusseau.

Catastrophe models are also still based upon historical data. Many have not been updated to account for the impacts of climate change, let alone cast forward to how flood risk may change in the future.

“The insurance industry drives using only the rearview mirror. Yesterday’s data to price tomorrow’s risks doesn’t work in a world of more extremes, says Vice President of Science Dr. Christopher Schwalm, who also contributed to the paper. “The past is no longer a reliable guide for the future. To stay ahead, we have to stop guessing based on what happened years ago and start modeling the ‘new extremes’ we are seeing right now.”

Informing policies that protect people

Dusseau along with Woodwell’s risk and policy experts have made science-backed contributions to conversations about improving flood insurance. Dusseau and Senior Policy Analyst Jamie Cummings authored a policy brief last April that advocates for NFIP reforms that help property owners access affordable flood protection, including the creation of a standard national catastrophe model. Dusseau has also briefed congressional staff, highlighting areas where Congress could play a role in bolstering the long-term resilience and insurability of communities.

Dominick Dusseau answers questions during a congressional briefing.

photo courtesy of Environmental and Energy Study Institute

However, aligning pricing more closely with the realities of climate change is much more complicated—and for many property owners, emotional—than simply incorporating the right data. The increases brought on by Risk Rating 2.0 have already pushed flood insurance out of the range of affordability for many policy holders, forcing them to drop their coverage. The pricing framework is a sticking point in lawmakers’ debates over reauthorizing the NFIP in the long term. The program is currently funded through September 30, 2026.

“How do you balance updating policies to reflect true climate risk with affordability, in a political context? Yes, you want people to know that they’re in a flood zone, but if you price them out of the market, are you really helping them?” says Woodwell Climate Vice President of Policy and Government Relations Laura Uttley. “That’s why the work Woodwell’s risk team does is so vital. The science and modeling they provide adds context for the development and implementation of new policies. We are very pragmatic about the ways we recommend change.”

Additionally, federal policy changes happen much slower than climate ones, making it a challenge to build policy that is both durable and versatile.

“Policy change at the federal level can be incredibly slow. We need to consider policy proposals that build durable systems that enable adaptability, recognizing the urgency posed by rapidly changing conditions,” says Uttley.

Woodwell Climate has been involved in advocacy around the inclusion of flooding from extreme rainfall—called pluvial flooding—in FEMA’s regulatory maps. These maps identify “flood hazard zones” in which property owners are required to have flood insurance. Currently they only represent coastal and riverine flooding hazards. This has led many property owners to mistakenly believe their homes are not at risk.

Though improved data and transparency might ultimately translate to higher costs for some, Dusseau says the alternative, not knowing, hurts people in the long run.

“If people don’t know that they’re at high risk, they won’t know what to do about it so they won’t do anything about it,” says Dusseau.